Supply and Demand#

One of the most basic and fundamental concepts in economics is the supply and demand model. Supply and demand represent the relationship between the quantity supplied that producers wish to sell at a certain price and the quantity demanded by consumers. In a free market, the prices for a certain good or service is determined by the supply, the demand, as well as various other factors. The relationship between the supply and demand of a good versus the price of a good is described by two of the most fundamental and important laws in microeconomics: the law of supply and the law of demand.

Law of Supply#

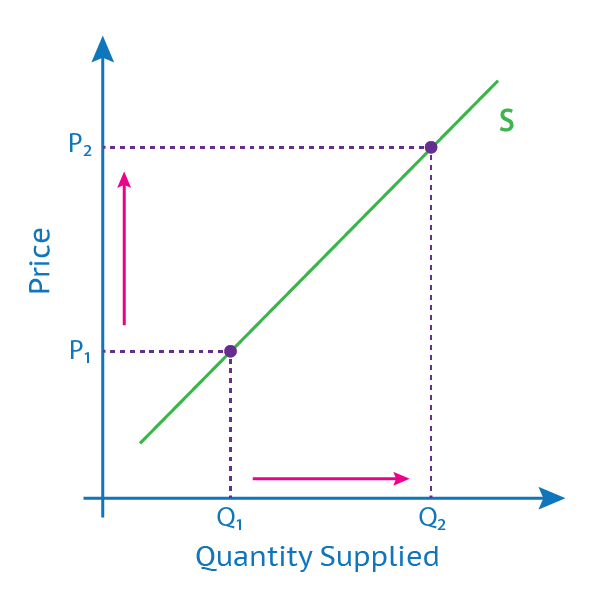

The law of supply holds that, ceteris paribus, the supply for a good changes inversely according to the price of the good. In other words, increased prices means higher amount of supply, decreased prices means lower demand. This is because when prices are higher, suppliers are incentivized supply more of that product, as it would have comparatively higher profit margin compared to other products. Lower prices reduce supply, as suppliers will decide to concentrate more of their resources to produce products which have a higher profit margin.

Graph which demonstrates the law of supply.#

Law of Demand#

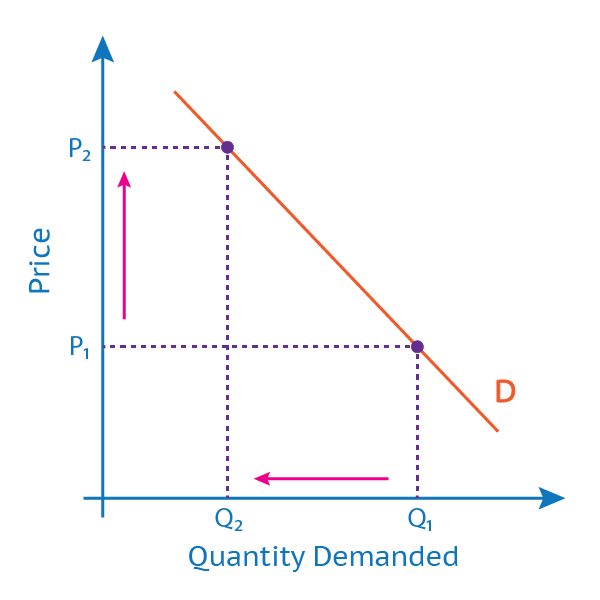

The law of demand holds that, ceteris paribus, the demand for a good changes with the price of the good. This is because consumers only have a finite amount of resources, and the amount that they spend on buying a particular product is limited. As such, increased prices means lower demand, and decreased prices means higher demand. Additionally, if they deem the price of the product too great, they will search for a substitute good.

Of course, there are exceptions to this rule. Luxury goods, sometimes also known as Veblen goods, are luxury goods which gain value. When prices go up, their demand subsequently rises because the price of the luxury goods is often used as a symbol for the owner’s wealth and social status.

Graph which demonstrates the law of demand.#

Equilibrium#

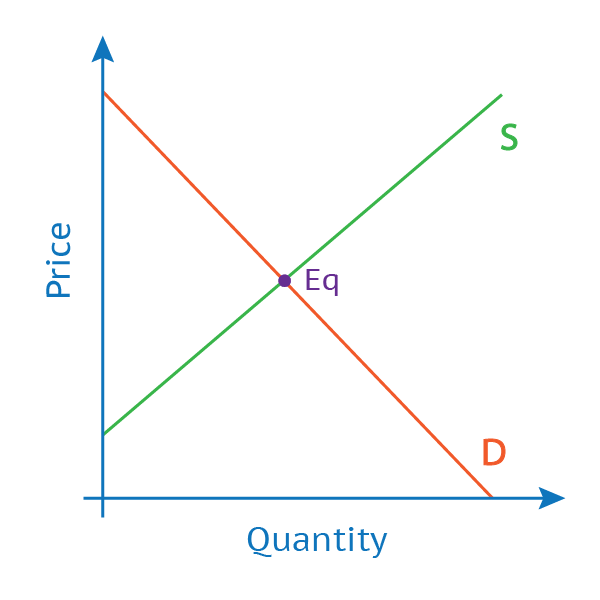

The intersection points of the supply curve and the demand curve is the equilibrium, or market-clearing price. This is an economic state is where markets are the most efficient, as it means that there is no surplus supply or unmet demand. However, equilibrium is seen as a theoretical concept and not a realistic goal, as it is extremely unlikely that all the economic conditions are exactly balanced to result in supply being exactly equal to demand.

Graph which demonstrates that the equilibrium point is the intersection of the supply curve and the demand curve.#

Types of Shifts#

A shift is when a change in demand or supply occurs, which has both short-term and long-term impacts on price, quantity demanded, and/or quantity supplied of a product. Shifts can be categorized into 2 types: price shifts and non-price shifts.

Price Shifts#

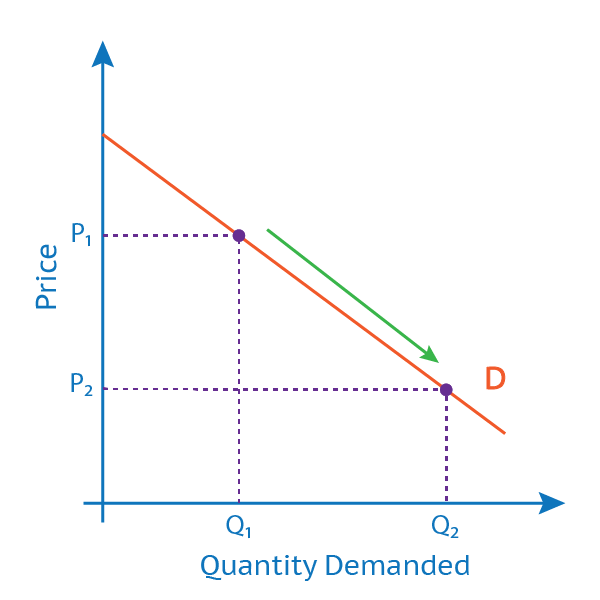

A price shift describes a change in price, which causes a change in the quantity demanded or supplied. Price shifts happen on the curve, and they do not cause a translation of the curve. As we can see from the example graph below, a change in price from \(P_1\) to \(P_2\) causes the quantity demanded of the good change from \(Q_1\) to \(Q_2\).

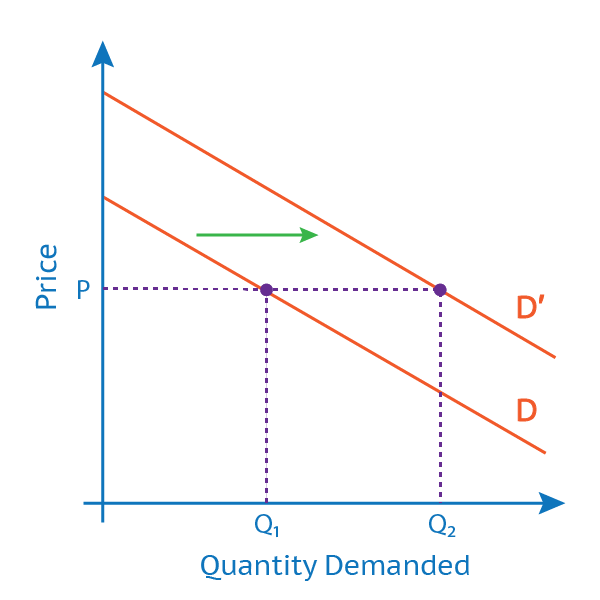

Non-price Shifts#

Non-price shifts describes a fundamental change in demand or supply which affects the behavior of suppliers or buyers. Non-price translates the entire curve, meaning that the quantity supplied or demanded has changed at every single price point. As we can see from the example graph below, a non-price shift has resulted in the quantity demanded to shift from \(Q_1\) to \(Q_2\), despite the fact that they are priced at the same price point \(P\).

Shifters of Supply and Demand#

Shifters of supply and demand (sometimes also known as determinates of supply and demand) are non-price shifts which affect the supply and/or the demand of a good or service. Shifters play an important role in shaping the economy, and understanding the effects that each shifter could have on the economy helps us understand and predict trends within an economy. Understanding these factors also allows suppliers, consumers, governments to make informed decisions on what to produce, and what to buy.

Shifters of Demand#

Tastes and Preferences - social trends could cause a product to suddenly spike demand. For example, if fidget spinners suddenly become very popular, the demand for it will spike, because everyone wants it.

Number of Consumers - if the amount of target consumers for a certain good increases, the demand of the product will increase. For example, if there is a sudden influx of migrants, housing prices will spike.

Price of Related Goods - if the price or demand of a related good changes, it could affect the price and demand of similar goods. For example, if a brand of shoes suddenly lowered the prices drastically, the demand for other brands of shoes will drop because people want to buy cheaper shoes.

Income - the amount of money each household makes affects the amount of money they spend. For example, if an economic recession throws people out of work, the demand for cars will decrease significantly, because people cannot afford to buy cars.

Speculation - people’s expectations for the performance of a market can affect the price or demand of a good. For example, if people loose trust in the Turkish lira, they will sell their lira for other currency, causing the value of the lira to drop.

Shifters of Supply#

Profit Margin - if there is more profit to be made by selling a certain product, suppliers will supply more of that product in order to increase their profit. For example, if there is a shortage of oil, people will be more willing to pay a higher price for oil, and as such the profit per barrel of oil for suppliers will increase, causing them to supply more oil. This also has the effect of bring the oil prices back down, due to the rise in supply in the market.

Cost of Production - if it becomes more expensive to produce a certain good, suppliers will allocate their resources to produce goods that are profitable, causing a decrease in supply. For example, if the price of wood increases significantly, artisans might move to other more profitable domains, resulting in a decrease in supply.

Availability of Raw Materials - if a resource required to make a certain good suddenly becomes scarce, suppliers can only make a limited amount of supply due to limited resources. For example, if there is a shortage of silicon ore, this could limit the supply of silicon wafers, causing a semiconductor shortage.

Competition - the competition between suppliers to create cheaper and higher quality products leads to higher demand, which results in an increase in demand to meet that demand.

Speculation - people’s expectations for the performance of a market can affect the price or supply of a good. For example, if people expect an economic recession, businesses will lower their production level in order to maintain low operational risks.

Government intervention - this can either come in the form of subsides, which help the industry and increasing supply, or in the form of price controls, which could either increase or decrease supply.

See also